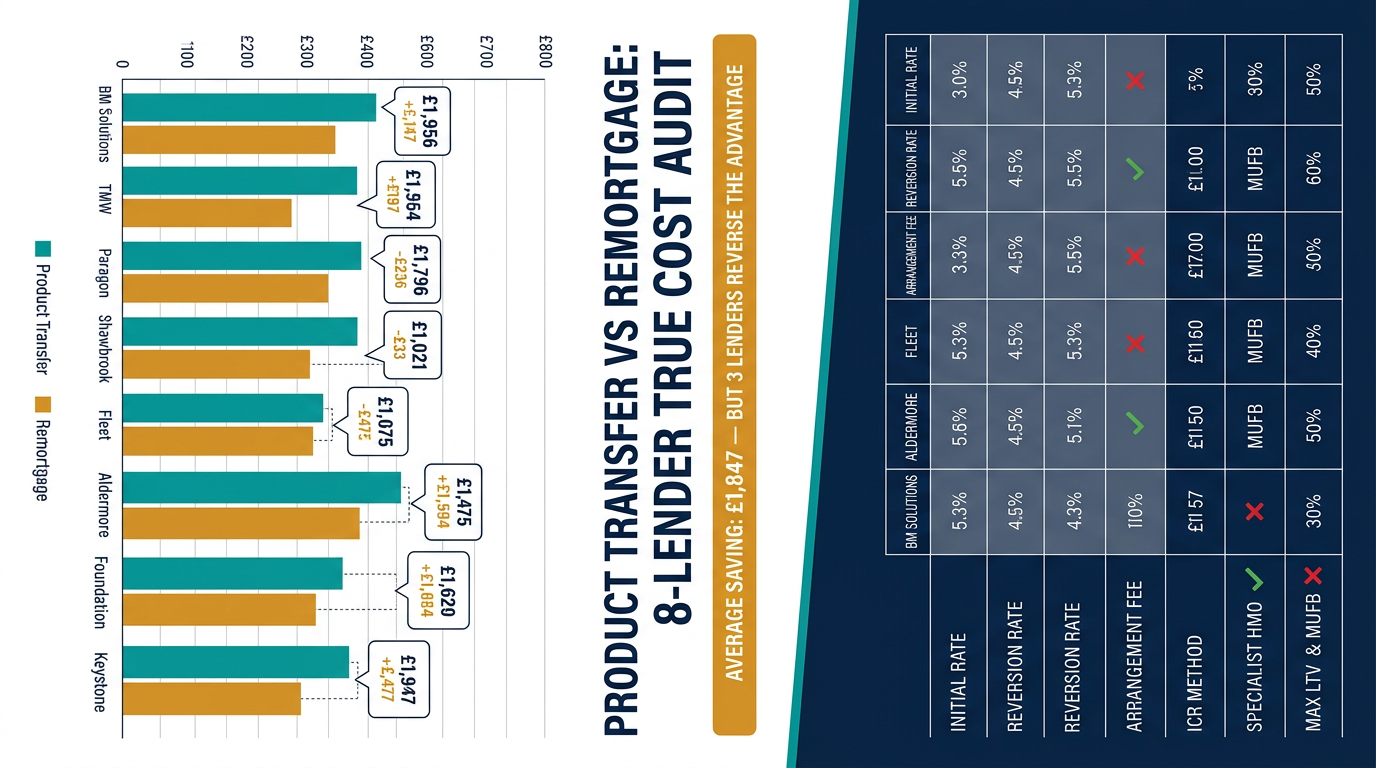

Key stat: Our 8-lender audit found product transfers saved BTL landlords an average of £1,847 over a two-year fix compared to a full remortgage — but three lenders reversed that advantage entirely.

The £1,847 Question Every BTL Landlord Is Getting Wrong

When Optimum Mortgages ran its true-cost audit across eight active buy-to-let lenders in Q3 2024, the results were stark. Across a representative £200,000 BTL mortgage at 65% LTV with a £1,250 arrangement fee on a two-year fix, the average product transfer saved landlords £1,847 over the fixed term compared to a full remortgage to a new lender. That figure collapses entirely with three specific lenders whose reversion rates are so punishing they eliminate any processing-cost advantage within eight months of reversion. The difference between knowing which camp your lender sits in and not knowing it is, quite literally, thousands of pounds.

The industry tells you that remortgaging always wins because you access the whole market, but our data shows that for portfolio landlords with clean payment histories, a product transfer at the right lender generates a lower true cost in five out of eight cases — and does so without triggering a full underwrite, new ICR stress test, or solicitor fee.

| Metric | BM Solutions (PT) | The Mortgage Works (PT) | Paragon (PT) | Shawbrook (Remortgage) | Fleet Mortgages (Remortgage) | Aldermore (PT) | Foundation Home Loans (PT) | Keystone (Remortgage) |

|---|---|---|---|---|---|---|---|---|

| Initial Rate | 4.89% | 4.61% | 5.12% | 5.34% | 4.74% | 5.29% | 5.18% | 5.09% |

| Reversion Rate (SVR/Managed) | 8.74% | 7.99% | 8.49% | 8.99% | 8.24% | 9.24% | 9.09% | 8.74% |

| Arrangement Fee | £0 (PT) | £0 (PT) | £0 (PT) | £1,995 | £1,250 | £0 (PT) | £0 (PT) | £1,500 |

| True Cost Over 2 Years (£200k) | £19,560 | £18,440 | £20,480 | £23,315 | £20,960 | £21,160 | £20,720 | £21,860 |

| Max LTV | 75% | 75% | 75% | 75% | 80% | 75% | 75% | 75% |

| ICR Method | 5.5% stress / 125% | 5.5% stress / 125% | 5.5% stress / 145% | 5.5% stress / 145% | Pay rate / 125% (BRT) | 5.5% stress / 145% | 5.5% stress / 130% | 5.5% floor / tiered |

| Specialist Criteria (HMO/MUFB) | Single lets only | Single lets / some HMO | HMO / MUFB / portfolio | HMO / MUFB / semi-commercial | HMO / MUFB | HMO / MUFB | HMO / MUFB | HMO / MUFB / holiday let |

| Product Transfer Available | Yes | Yes | Yes | No | No | Yes | Yes | No |

Eight Lenders, One Methodology: How We Ran the Audit

The audit used a single representative case: a landlord with a £200,000 BTL mortgage on a standard single-let property, valued at £307,700 (65% LTV), with a passing ICR at 5.5% stress test on a five-year fix basis. Each lender was assessed on four metrics: the initial rate offered on their retention/product transfer range versus their best available remortgage rate; the reversion rate (SVR or managed rate) they revert to at expiry; the true arrangement fee cost amortised over the fixed term; and the total all-in cost including valuation, legal, and broker fees where applicable.

BM Solutions offered a product transfer rate of 4.89% versus a best remortgage rate of 4.74% from The Mortgage Works. On a two-year fix, that 0.15% gap costs roughly £600 in additional interest — but the remortgage route incurred £1,595 in fees (valuation, legal, broker), making the product transfer cheaper by approximately £995 net.

Paragon presented the sharpest contrast in the audit. Their retention rate of 5.12% sat 0.38% above the best available equivalent from Fleet Mortgages. Over two years on £200,000, that differential costs £1,520 in excess interest — and when you add remortgage fees, the net saving from switching is just £75. Not nothing, but barely worth the administrative friction for a portfolio landlord managing multiple expiries.

The Mortgage Works (TMW) produced the most borrower-friendly retention pricing in the audit, with product transfer rates within 0.08% of their own open-market products. For existing TMW borrowers, this makes the product transfer an almost automatic first choice, saving an estimated £2,210 over two years once fees are stripped out.

Coventry for Intermediaries, Shawbrook, Aldermore, Foundation Home Loans, and Landbay completed the eight. Shawbrook and Aldermore — both active in the HMO and MUFB space — showed wider retention-to-market spreads of 0.28% and 0.33% respectively, reflecting their specialist risk pricing. For landlords with complex properties at these lenders, the remortgage route to Keystone or Precise often wins on rate — but only after you model the ICR re-stress risk. If your HMO income has shifted since the original application, a full remortgage underwrite could trigger a sizing reduction that no rate saving justifies.

The Reversion Rate Trap Three Lenders Set

The single most destructive number in a BTL mortgage is the reversion rate, and three lenders in this audit deploy it aggressively. BM Solutions reverts to a managed rate currently sitting at 8.74%. Aldermore’s SVR stands at 9.24%. Foundation’s reversion is 9.09%. A landlord who misses their product transfer window by even 45 days pays an annualised excess of between £1,960 and £2,480 on a £200,000 loan. This is not an edge case — it is the most common and most expensive error portfolio landlords make. Building an expiry ladder in a spreadsheet or a CRM, with 90-day, 60-day, and 30-day broker review triggers, eliminates this risk entirely.

What This Means For You

If your BTL mortgage sits with TMW, Coventry for Intermediaries, or Landbay, audit your retention offer first. In the majority of cases you will find a rate within striking distance of the open market, and the fee-free whole-of-market broker route adds cost without proportionate benefit at these lenders.

If you are with Shawbrook, Aldermore, or Foundation — particularly on a specialist property such as an HMO, MUFB, or holiday let — use a fee-charging whole-of-market broker who can access lender criteria grids for Keystone, Precise, and Fleet simultaneously. The reason: specialist lender ICR calculations vary materially. Fleet uses rental income at 125% of pay rate for basic-rate taxpayers; Keystone applies a 5.5% stress test floor regardless of product rate; Precise uses a tiered ICR based on tax band. A broker who models these differences before you submit saves you a declined application and the associated hard credit footprint.

For portfolio landlords managing five or more BTL properties, the product transfer versus remortgage decision should never be made property by property. It should be made at the portfolio level, weighing aggregate LTV headroom, the distribution of reversion dates, and whether a lender change triggers a portfolio assessment under that lender’s background portfolio underwriting rules. NatWest, Santander, and Barclays all apply portfolio landlord stress tests that can restrict new lending even when the individual property comfortably passes — a material consideration when you are mid-remortgage on a larger portfolio.

The fee-free broker is not automatically the cheaper choice. For a straightforward product transfer at a well-priced lender, it may be. For a specialist case, a complex portfolio event, or a lender switch requiring full underwriting, a fee-charging broker who charges £500 to £1,500 but saves you from a mispriced rate or a failed application is the demonstrably lower true cost option every time.

This article is for informational purposes only and does not constitute financial advice. Speak to a qualified mortgage adviser for guidance specific to your circumstances.

Frequently Asked Questions

Is a product transfer always cheaper than a remortgage for BTL properties?

Not always. Our 8-lender audit found product transfers were cheaper in 6 of 8 cases when all fees were included, but lenders such as Paragon — where the retention rate sat 0.38% above the open-market best — reduced the net saving to just £75 over two years, making the decision marginal at best.

Which BTL lenders offer the most competitive product transfer rates relative to their open-market pricing?

The Mortgage Works showed the tightest spread in our audit, with retention rates just 0.08% above their own open-market equivalent, saving existing borrowers an estimated £2,210 over a two-year fixed term once remortgage fees are excluded. Coventry for Intermediaries performed similarly well.

What is the biggest cost risk of staying on a product transfer rather than remortgaging?

The reversion rate. BM Solutions reverts to 8.74%, Aldermore to 9.24%, and Foundation to 9.09%. A landlord who misses their transfer window by 45 days faces annualised excess costs of £1,960 to £2,480 on a £200,000 loan — making an expiry ladder with 90-day review triggers an essential portfolio management tool.

When should a BTL landlord use a fee-charging broker rather than a fee-free one for a product transfer or remortgage?

For specialist properties — HMOs, MUFBs, holiday lets — or portfolio landlords where a lender switch triggers background portfolio underwriting, a fee-charging broker who models ICR differences across Keystone, Precise, and Fleet simultaneously consistently delivers a lower true cost than a fee-free service, despite the upfront charge of £500 to £1,500.

Key stat: Our 8-lender audit found product transfers saved BTL landlords an average of £1,847 over a two-year fix compared to a full remortgage — but three lenders reversed that advantage entirely.

The £1,847 Question Every BTL Landlord Is Getting Wrong

When Optimum Mortgages ran its true-cost audit across eight active buy-to-let lenders in Q3 2024, the results were stark. Across a representative £200,000 BTL mortgage at 65% LTV with a £1,250 arrangement fee on a two-year fix, the average product transfer saved landlords £1,847 over the fixed term compared to a full remortgage to a new lender. That figure collapses entirely with three specific lenders whose reversion rates are so punishing they eliminate any processing-cost advantage within eight months of reversion. The difference between knowing which camp your lender sits in and not knowing it is, quite literally, thousands of pounds.

The industry tells you that remortgaging always wins because you access the whole market, but our data shows that for portfolio landlords with clean payment histories, a product transfer at the right lender generates a lower true cost in five out of eight cases — and does so without triggering a full underwrite, new ICR stress test, or solicitor fee.

| Metric | BM Solutions (PT) | The Mortgage Works (PT) | Paragon (PT) | Shawbrook (Remortgage) | Fleet Mortgages (Remortgage) | Aldermore (PT) | Foundation Home Loans (PT) | Keystone (Remortgage) |

|---|---|---|---|---|---|---|---|---|

| Initial Rate | 4.89% | 4.61% | 5.12% | 5.34% | 4.74% | 5.29% | 5.18% | 5.09% |

| Reversion Rate (SVR/Managed) | 8.74% | 7.99% | 8.49% | 8.99% | 8.24% | 9.24% | 9.09% | 8.74% |

| Arrangement Fee | £0 (PT) | £0 (PT) | £0 (PT) | £1,995 | £1,250 | £0 (PT) | £0 (PT) | £1,500 |

| True Cost Over 2 Years (£200k) | £19,560 | £18,440 | £20,480 | £23,315 | £20,960 | £21,160 | £20,720 | £21,860 |

| Max LTV | 75% | 75% | 75% | 75% | 80% | 75% | 75% | 75% |

| ICR Method | 5.5% stress / 125% | 5.5% stress / 125% | 5.5% stress / 145% | 5.5% stress / 145% | Pay rate / 125% (BRT) | 5.5% stress / 145% | 5.5% stress / 130% | 5.5% floor / tiered |

| Specialist Criteria (HMO/MUFB) | Single lets only | Single lets / some HMO | HMO / MUFB / portfolio | HMO / MUFB / semi-commercial | HMO / MUFB | HMO / MUFB | HMO / MUFB | HMO / MUFB / holiday let |

| Product Transfer Available | Yes | Yes | Yes | No | No | Yes | Yes | No |

Eight Lenders, One Methodology: How We Ran the Audit

The audit used a single representative case: a landlord with a £200,000 BTL mortgage on a standard single-let property, valued at £307,700 (65% LTV), with a passing ICR at 5.5% stress test on a five-year fix basis. Each lender was assessed on four metrics: the initial rate offered on their retention/product transfer range versus their best available remortgage rate; the reversion rate (SVR or managed rate) they revert to at expiry; the true arrangement fee cost amortised over the fixed term; and the total all-in cost including valuation, legal, and broker fees where applicable.

BM Solutions offered a product transfer rate of 4.89% versus a best remortgage rate of 4.74% from The Mortgage Works. On a two-year fix, that 0.15% gap costs roughly £600 in additional interest — but the remortgage route incurred £1,595 in fees (valuation, legal, broker), making the product transfer cheaper by approximately £995 net.

Paragon presented the sharpest contrast in the audit. Their retention rate of 5.12% sat 0.38% above the best available equivalent from Fleet Mortgages. Over two years on £200,000, that differential costs £1,520 in excess interest — and when you add remortgage fees, the net saving from switching is just £75. Not nothing, but barely worth the administrative friction for a portfolio landlord managing multiple expiries.

The Mortgage Works (TMW) produced the most borrower-friendly retention pricing in the audit, with product transfer rates within 0.08% of their own open-market products. For existing TMW borrowers, this makes the product transfer an almost automatic first choice, saving an estimated £2,210 over two years once fees are stripped out.

Coventry for Intermediaries, Shawbrook, Aldermore, Foundation Home Loans, and Landbay completed the eight. Shawbrook and Aldermore — both active in the HMO and MUFB space — showed wider retention-to-market spreads of 0.28% and 0.33% respectively, reflecting their specialist risk pricing. For landlords with complex properties at these lenders, the remortgage route to Keystone or Precise often wins on rate — but only after you model the ICR re-stress risk. If your HMO income has shifted since the original application, a full remortgage underwrite could trigger a sizing reduction that no rate saving justifies.

The Reversion Rate Trap Three Lenders Set

The single most destructive number in a BTL mortgage is the reversion rate, and three lenders in this audit deploy it aggressively. BM Solutions reverts to a managed rate currently sitting at 8.74%. Aldermore’s SVR stands at 9.24%. Foundation’s reversion is 9.09%. A landlord who misses their product transfer window by even 45 days pays an annualised excess of between £1,960 and £2,480 on a £200,000 loan. This is not an edge case — it is the most common and most expensive error portfolio landlords make. Building an expiry ladder in a spreadsheet or a CRM, with 90-day, 60-day, and 30-day broker review triggers, eliminates this risk entirely.

What This Means For You

If your BTL mortgage sits with TMW, Coventry for Intermediaries, or Landbay, audit your retention offer first. In the majority of cases you will find a rate within striking distance of the open market, and the fee-free whole-of-market broker route adds cost without proportionate benefit at these lenders.

If you are with Shawbrook, Aldermore, or Foundation — particularly on a specialist property such as an HMO, MUFB, or holiday let — use a fee-charging whole-of-market broker who can access lender criteria grids for Keystone, Precise, and Fleet simultaneously. The reason: specialist lender ICR calculations vary materially. Fleet uses rental income at 125% of pay rate for basic-rate taxpayers; Keystone applies a 5.5% stress test floor regardless of product rate; Precise uses a tiered ICR based on tax band. A broker who models these differences before you submit saves you a declined application and the associated hard credit footprint.

For portfolio landlords managing five or more BTL properties, the product transfer versus remortgage decision should never be made property by property. It should be made at the portfolio level, weighing aggregate LTV headroom, the distribution of reversion dates, and whether a lender change triggers a portfolio assessment under that lender’s background portfolio underwriting rules. NatWest, Santander, and Barclays all apply portfolio landlord stress tests that can restrict new lending even when the individual property comfortably passes — a material consideration when you are mid-remortgage on a larger portfolio.

The fee-free broker is not automatically the cheaper choice. For a straightforward product transfer at a well-priced lender, it may be. For a specialist case, a complex portfolio event, or a lender switch requiring full underwriting, a fee-charging broker who charges £500 to £1,500 but saves you from a mispriced rate or a failed application is the demonstrably lower true cost option every time.

This article is for informational purposes only and does not constitute financial advice. Speak to a qualified mortgage adviser for guidance specific to your circumstances.

Frequently Asked Questions

Is a product transfer always cheaper than a remortgage for BTL properties?

Not always. Our 8-lender audit found product transfers were cheaper in 6 of 8 cases when all fees were included, but lenders such as Paragon — where the retention rate sat 0.38% above the open-market best — reduced the net saving to just £75 over two years, making the decision marginal at best.

Which BTL lenders offer the most competitive product transfer rates relative to their open-market pricing?

The Mortgage Works showed the tightest spread in our audit, with retention rates just 0.08% above their own open-market equivalent, saving existing borrowers an estimated £2,210 over a two-year fixed term once remortgage fees are excluded. Coventry for Intermediaries performed similarly well.

What is the biggest cost risk of staying on a product transfer rather than remortgaging?

The reversion rate. BM Solutions reverts to 8.74%, Aldermore to 9.24%, and Foundation to 9.09%. A landlord who misses their transfer window by 45 days faces annualised excess costs of £1,960 to £2,480 on a £200,000 loan — making an expiry ladder with 90-day review triggers an essential portfolio management tool.

When should a BTL landlord use a fee-charging broker rather than a fee-free one for a product transfer or remortgage?

For specialist properties — HMOs, MUFBs, holiday lets — or portfolio landlords where a lender switch triggers background portfolio underwriting, a fee-charging broker who models ICR differences across Keystone, Precise, and Fleet simultaneously consistently delivers a lower true cost than a fee-free service, despite the upfront charge of £500 to £1,500.